Taking Money from your Ltd Company

As an owner-director of a UK Ltd company, your objectives include minimising both your business taxes and personal tax liabilities. A question you may be asking yourself is: how do I take money out of my Ltd company for personal use in a tax-effective manner?

Below are some considerations to discuss with your accountant or financial advisor to determine the best strategy for you. This guidance assumes you are an owner and director of a UK Limited Company with income exclusively from your Ltd Company. If you have other sources of income, implementing some of the below strategies may still be beneficial – again, consult your financial advisor.

Generally, a combination of salary and dividends from your Ltd company is recommended, as outlined below.

- Take a salary up to the level of the personal allowance – £12,570.00 for the 2025/26 tax year.

- Take the remainder of what you need as dividends.

This is not a one-size-fits-all situation but will be suitable for some companies and directors.

Take a Small Salary up to the Personal Allowance Limit

The personal allowance for the 2025/26 tax year is £12,570.00.

When you pay yourself a salary from your company, it reduces your company’s profit, thus lowering your corporation tax liability. Salaries are a tax-deductible expense for corporation tax.

It is advisable to keep your salary at or below the personal allowance figure to avoid income tax (PAYE) and Employee National Insurance Contributions (NICs), for which you would incur on amounts above the personal allowance.

The thing to note about your personal allowance is that it is a “use it or lose it” situation. If you do not utilise it in a given tax year, you cannot carry it forward to the next. It is tax-free income that you should try to take advantage of. You may wish to leave the money (your salary) in your company, which is fine; your salary can be coded to your director’s loan account – meaning you won’t actually pay yourself the money at this time, allowing the business to use the funds for now. You will be building up a pot of money in your director’s loan account that you can draw from tax-free in future.

As the employee receiving the salary you will pay no income tax (PAYE) or national insurance contributions on a salary that is equal to or below the personal allowance.

The company will have to pay some Employer NICs (15% for the 2025/26 year) on anything you earn above the NIC secondary threshold (which, in the 2025/26 tax year is £5,000.00).

So, in our example above, the company would pay 15% NICs on the portion of the salary paid above the NIC secondary threshold:

£12,570.00 – £5,000.00 = £7,570.00

NIC payable will be £7,570.00 x 15% = £1,135.50

Note – employer NICs are also a tax-deductible expense for corporation tax.

You might wonder why not just pay yourself a lesser salary to avoid employer NICs. Here are a few reasons:

1. Meeting NIC requirements for the state pension: If you pay yourself a salary below the NIC secondary threshold (£5,000.00 for the 2025/26 tax year), you also earn below the Lower Earnings Limit for NICs (£6,500.00 in 2025/26), potentially affecting your eligibility for a qualifying year of NIC payments, and consequently, your future state pension.

2. Corporation tax savings: Paying a lower salary results in higher company profits and thus higher corporation tax. By paying a salary of £12,570.00:

- You will pay 15% on the £7,570.00 in employer NICs. However, your company doesn’t pay corporation tax on the £7,570.00 or the £1,135.50 for the employer NICs, as these are tax-deductible for corporation tax.

- £7,570.00 + £1,135.50 = £8,705.50

- By doing so, you save £1,654.05 in corporation tax: £8,705.50 x 19% = £1,654.05 (19% is the small profits rate for corporation tax: 2025/26 tax year).

Another way to view it is that paying NICs on the salary portion above the NIC secondary threshold at 15% is cheaper than paying 19% corporation tax on that money.

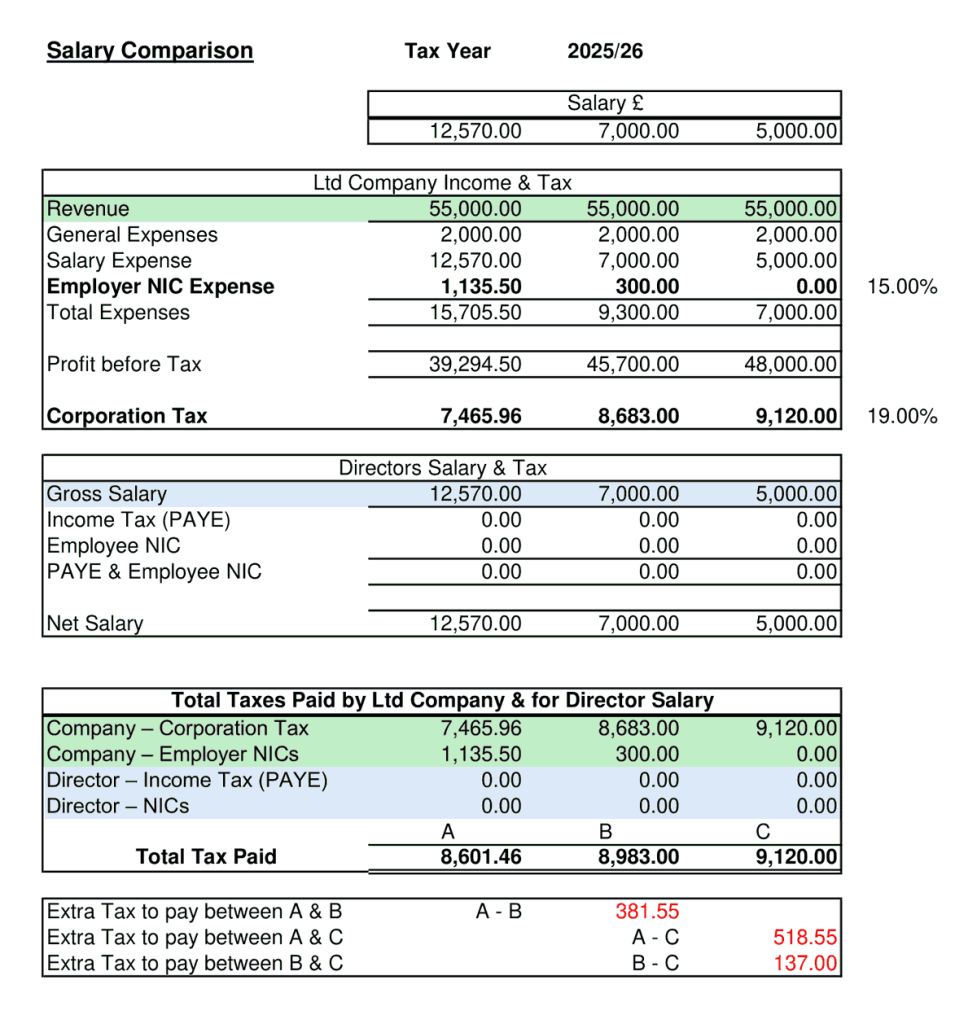

See the table below to show a comparison example for yearly salaries of £12,570.00, £7,000.00, £5,000.00 and the overall tax paid–saved – 2025/26 tax year.

What if you’re unsure about regular salary payments?

If you’re just starting with your Ltd company or are concerned about cash flow, you might wonder if you’ll have enough money to pay a regular salary.

You can still run your payroll each month without physically paying the salary out to yourself – simply code the payment to your Director’s Loan Account as a liability the company owes you. When you do make a profit, you have money available in your director’s loan account that you can draw on tax-free.

Caution – you must ensure you have enough money to pay your monthly Employer NICs to HMRC.

Take Dividends Alongside Your Salary

You can take dividends from your Ltd company in addition to your salary. Dividends are not subject to employer or employee NICs. Generally, it is more tax-efficient to take a small salary (as stated above) and then take the rest as dividends.

You can also take advantage of the Dividend Allowance, allowing you to receive a small amount of dividends each year tax-free. For the 2025-26 year, the dividend allowance is £500.00.

You must hold a board meeting to discuss and agree on the dividend distribution and record this in the minutes – even if you are the sole director/shareholder. Additionally, you must issue a dividend certificate and keep a record. While this process is straightforward, your accountant or financial advisor can assist.

Notes:

- Dividends can only be paid out from business profits – it is illegal to take dividends if the business has no profits.

- Dividends are not tax-deductible for corporation tax.

Consider Pensions

Paying money into a private pension (subject to certain limits and legislative compliance) is another way to move money out of your company efficiently. Employer pension contributions are tax-deductible for corporation tax. Also, as an employee, you can get tax relief on your pension contributions.

Summary

These are some ways to draw money from your Ltd company in a tax-efficient manner, but they are not the only means. This overview is given to provoke thought and discussion with your accountant or financial advisor.

Again – this is not a one-size-fits-all situation but will be suitable for some companies and directors.

Disclaimer: The content on our site is for general information only and not professional advice. Always seek professional guidance before acting on any information here. While we strive for accuracy, we cannot guarantee completeness or timeliness of the content.